Welcome to our weekly roundup of news from South America.

Mosoj ESG provides information, data and analyses relating to South America integrating Environmental, Social and Governance topics to promote sustainable development.

Lithium - the new marching powder

This week we came across an online event on lithium ion battery and EV supply chain. The main takeaways were that (i) demand for lithium is about to expand exponentially, and (ii) supply is a risk - given location of resources and supply-to-market time.

So what is lithium? Traditionally, lithium minerals were mostly used in industrial applications, including ceramics, glass and aluminium production. By 2020, it became mostly used in rechargeable batteries for portable electronic devices, and EV batteries.

The latter drove much investment to increase extraction, so much so that by 2017 production had overtaken consumption by a fair margin. As the expectation was that consumption would catch up, prices reached an all-time high in 2018 for lithium carbonate of 17,500 usd/ tonne, before falling abruptly to just over 5,000 usd/tonne.

Source: USGS

This in part explains some of the financial problems faced by lithium players like Tianqi Lithium, while others have difficulties accessing the necessary financing to increase their production capabilities, as supply continues to exceed demand.

This is set to change in a post-Covid world as many countries around the world announced their intention to become carbon neutral over the next decades, e.g. China has a net-zero target for 2060, as well as several European countries.

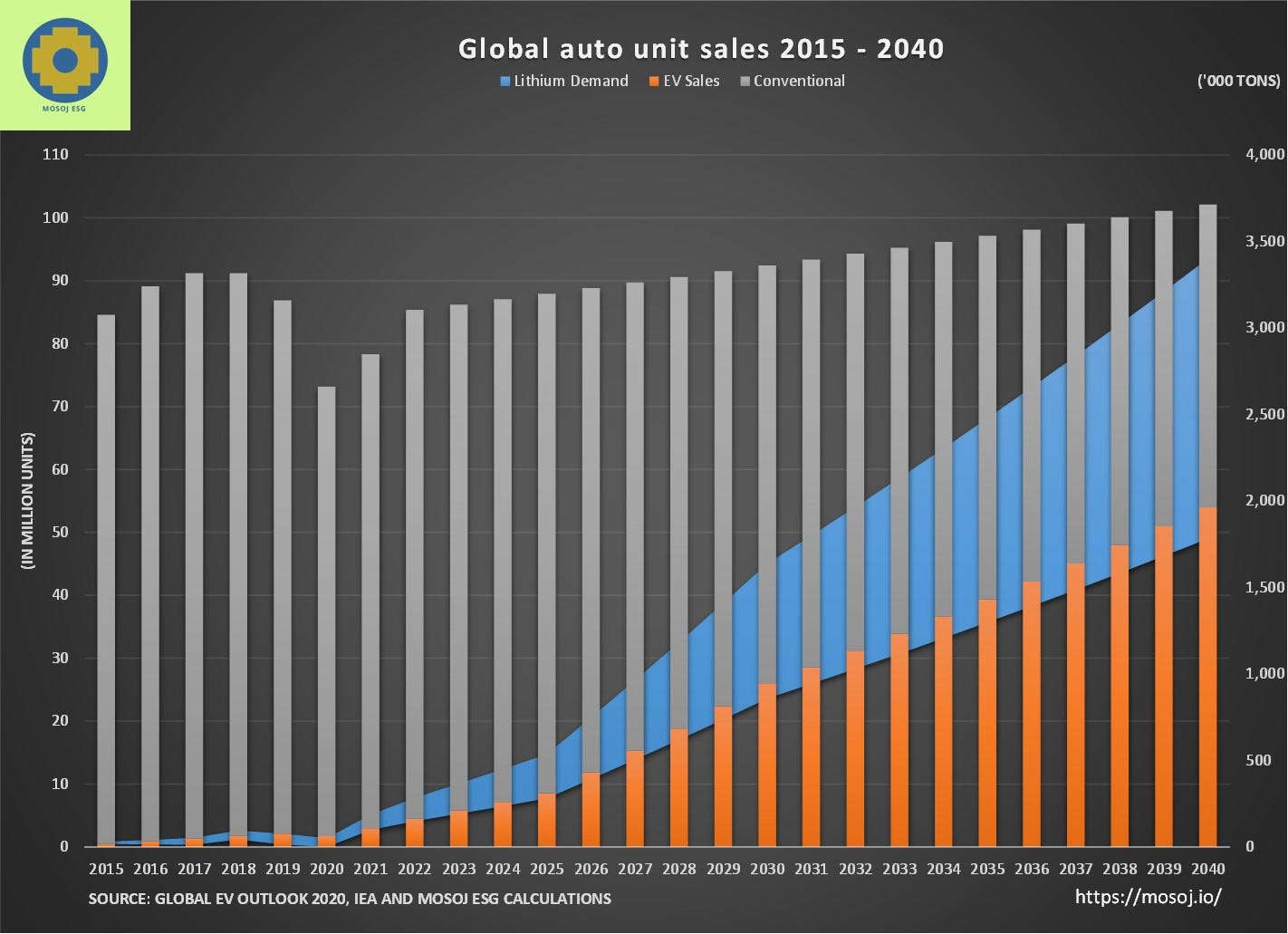

For sure, many expects the automobile industry to be radically altered as a result of this shift away from fossil fuels, and therefore internal combustion engine (ICE). Current forecasts predict that electric vehicles (EVs) will account for almost 50% of all car sales by 2040. This could be an underestimation, especially when looking at the stock-market valuation of EV companies such as Tesla ($578bn) vs Toyota ($209bn) .

Source: Global EV Outlook 2020, IEA and Mosoj ESG calculations

As many car manufacturers start their production of EVs, demand for lithium batteries is expected to sky-rocket. It is noteworthy that policymakers are also expected to be a big driver of this shift away fossil fuels, with possible carbon taxes on ICE vehicles.

Thus, overall the outlook for lithium demand appears pretty bullish, whatever way you look at it. Certainly, if any of the above prediction regarding the penetration rate of EVs is true, lithium resource-rich countries should benefit immensely.

For some South American countries, it could be significant, as 60% of the world resources is located in Bolivia (21 million metric tons), Chile (17 million metric tons) and Argentina (12 million metric tons). As such, we should expect massive investments in these countries by companies whose end-market is China, the US and Europe.

World Resources - million tons

Source: USGS

So far, however, most of global lithium production has been located at just six mineral operations in Australia, two brine operations each in Argentina and Chile, and one brine and one mineral operation in China.

Australia is the world´s biggest producer, with 42 Kt in 2019, and together with Chile and China, the three countries represent ca. 88% of global production.

Source: USGS

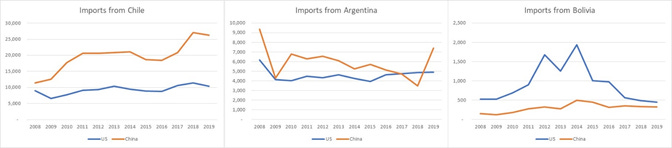

Of note, as China is fairly present both in Zimbabwe and Argentina, it would seem that China is ahead in the race to secure their supply of lithium. As such, we believe that this should be viewed as a source of geopolitical risk as other major powers – the US and EU, amongst others - will also need to secure their supply.

For sure, Chile – economically speaking – is already very much tilted towards China who is importing a growing amount of goods compared to the US, while Argentina appears to be following the same track. Bolivia on the other hand currently remains more linked to the US in terms of trade than to China, but this could change.

Source: Mosoj ESG, World Bank data

Going forward, as the decarbonisation of the economy leads to the electrification of society as a whole, many see lithium as the new white gold, and possibly as the new dominant source of our energy needs. It is therefore likely to have some influence over the politics and economic strategies of nations or economic groups (e.g. EU). For producing nations, it may prove a bonanza as well as a source of instability or dispute.

Finally, there appear to be many risks attached to the supply of lithium, mostly found in notoriously volatile environment. Indeed, it can take a long time for supply to come to market and there is currently a shortage of financing to increase supply.

As such, improving lithium-to-market time will be vital for a successful roll-out of EVs across the world. Indeed, raw material deficits would certainly lead to much higher prices that would be passed on the EV manufacturers and ultimately consumers, thereby disrupting adoption rates.

Brazilian corn exports rise 44% in the 1st week of December

Deforestation in the Amazon falls 45% in November, says Defense

Iata raises to $13.6 bn projection of revenue loss of airlines in Brazil

Executive Branch allocates $800 mm credit for Kandir Law agreement

E-commerce in the State of São Paulo will grow 32% in 2020, says FecomercioSP

Minas Gerais breaks a record and exceeds 800 MW installed in solar

BBCE operations grow 83.1% in November

CPFL announces $360 mm for sustainable transition by 2024

Energy distributor CEB was privatised with a $490 mn bid from a Neoenergia group company

FIDE says economy will grow 5.6% in 2021

Covid-19: Individuals with fortunes over $2.5mn will have to pay wealth tax

Tecpetrol will invest $1.5 billion for the next four years

Government exchanges securities for $750 million to compress exchange rate gap

Grimoldi: sales dropped 55%, and losses reached $6.08 mn in 9 months

Creditors to Argentina’s provinces fight to avoid painful restructurings of $15bn debt

Neo Lithium with an initial capital investment of $318.9mn

Andreani invests $60 million to expand its logistics business

Process to withdraw privately held pension funds to begin December 10th

Chile’s Central Bank forecasts economy to decrease by 5.75% to 6.25% in 2020

Chile’s consumer prices fall 0.1% in November

Meat shipments to Chile increased to 18,644 tons in November

Third Confucius Institute opens in Chile

Chile’s Codelco reaches labor deal with union at Radomiro Tomic mine

Tesoro Resources to raise $21M for exploration in Chile

Banco De Chile: Analyst consensus indicates potential 1.9% upside

Moody’s forecasts fiscal deficit at 7.6% of GDP and GDP growth at 4.8%

External debt in Colombia reached 52.6% of GDP as of September

Colombia gets green light for ESG bonds

Colombian households have lost income of $ 7.9 bn due to the pandemic

Internal conflict decreased tax collection in Colombia up to 10%

Added-value of construction sector in Colombia contracts by 26%

Moody’s affirms ratings of Colombian banks;

Colombian coffee production drops 4% in November

Bolivia’s Chamber of Commerce forecasts 4% growth in 2021

Bolivia received $873.7 mn in remittances until October

Beef exports to China grow 249.4%

Individuals with more than $4.4 mn in wealth will pay wealth tax

Bolívia’s Treasury will allocate $376.4mn to cover payment of Christmas bonus

Bolivia lost 27% of its Amazon forest between 2000 and 2018

Urea plant loses $257 million in one year and removes 84% of workers

International reserves reduced by $1.2 bn between September and November 2020